Caesars Entertainment properties in Las Vegas are Paris, shown in the background, as well as Bally’s, Bill’s, Flamingo, O’Sheas, Imperial Palace, Caesars Palace, Rio, Harrah’s and Planet Hollywood.

Monday, Feb. 15, 2010 | 2 a.m.

Jonathan S. Halkyard

Sun Coverage

Sun Archives

- Harrah’s gets OK for Planet Hollywood purchase; job cuts planned (2-3-10)

- Harrah’s to take over Planet Hollywood management (1-15-10)

- Harrah’s moves ahead with possible Planet Hollywood acquisition (11-30-09)

- Harrah’s working on plan to take over Planet Hollywood (11-25-09)

- Planet Hollywood’s financial outlook worsens (11-16-09)

- Harrah’s buys Planet Hollywood debt (9-15-09)

- Harrah’s expects annual savings of $500 million (3-17-09)

- Harrah’s reports loss, says LV properties hit hard (3-13-09)

- Harrah’s announces plan to reduce debt burden (3-4-09)

- Strip building boom, buyouts were ill-timed, and many see more pain in ’09 (3-1-09)

- Harrah’s wants class-action suit over debt swap dismissed (2-27-09)

- Harrah's hit with class-action lawsuit over debt plan (2-16-09)

- Harrah’s seeking $740 million from credit line (2-13-09)

- Harrah’s makes cost-cutting moves (2-12-09)

Beyond the Sun

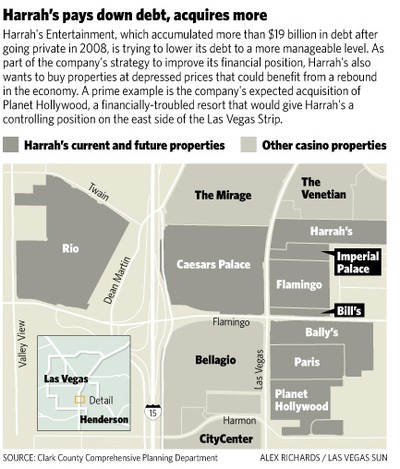

About a year ago, investors were so convinced that Harrah’s Entertainment would file for bankruptcy protection that the company’s bonds — its promises to pay back billions of dollars — traded for 10 cents on the dollar.

Since then, the world’s largest gaming company — one of the country’s biggest buyout targets during the real estate bubble — has surprised naysayers by carving out a foothold of three years during which it can afford to make interest payments on its debt. The hope is that by 2013, its earnings will be high again. They will need to be because that year a $6 billion debt payment will be due. Another $9 billion in debt, by analysts’ estimates, comes due between 2015 and 2019.

The 2008 leveraged buyout that took Harrah’s private doubled its debt — it has more debt than any other gaming company.

Harrah’s survival through at least 2013 can be traced to the work of fewer than two dozen people at a company that employs 55,000.

Although most of Harrah’s employees can only hope for the best while they are occupied with serving customers in a sorry economy, the job of whittling down more than $20 billion in debt has fallen to Chief Financial Officer Jonathan Halkyard, a 45-year-old Harvard MBA who has overseen a complex refinancing scheme some observers have called “a college course in credit.”

“Their financial engineering has been spectacular,” says Dennis Farrell, a bond analyst with Wells Fargo Securities.

Halkyard, one of the industry’s youngest CFOs, began his career with Chase Manhattan Bank in New York. He joined Harrah’s in 1999 as director of finance at Harrah’s Lake Tahoe, his first gaming job. He soon moved up to assistant general manager of Harrah’s and Harvey’s casinos at Lake Tahoe and later, assistant general manager of Harrah's Las Vegas.

Halkyard and his team’s work hasn’t been without controversy. Some analysts think the company, by extending the maturity dates on big chunks of debt, is simply delaying an inevitable outcome that might be preferable for the vast majority of Harrah’s employees. Although top executives typically lose their jobs and ownership in a company in bankruptcy, the process can wipe the slate clean of debt, enabling it to compete more effectively.

The more curious aspect of Halkyard’s approach is that in addition to postponing debt payments, the company appears to be on a spending spree.

Harrah’s expects to pay up to $100 million in cash to acquire the financially troubled Planet Hollywood on the Strip in addition to assuming the resort’s debt of $540 million — loans Harrah’s could delay paying until December 2015. It’s probably a bargain. The recently renovated resort is considered hip and cost more than $1 billion to build.

Still, some observers say this is risky for a company with lots of debt that generates nearly 40 percent of its earnings in Las Vegas and Atlantic City, the two most depressed casino markets.

In addition, Harrah’s has an option to buy an Ohio racetrack that could benefit if residents vote to legalize slot machines — a possibility that’s far from certain.

Harrah’s executives say now is the time to jump on cost-effective deals that will benefit from an economic rebound.

Buying low and selling high makes sense for cash-rich companies, not Harrah’s, argues Randall Fine, a casino consultant in Las Vegas and a former marketing executive for the company.

Buying Planet Hollywood is “foolish” because Harrah’s will need a significant improvement in business to stay afloat, Fine says.

“I believe you fix your problems before you take on more work. It’s like buying another house when you can’t afford the mortgage on the one you own.”

Harrah’s executives say they are in control of its finances. Profits have risen at properties purchased from competitors and added to the company’s widely emulated marketing program, Total Rewards, they say.

Halkyard speaks with the confidence of a gambler on a lucky streak.

“Given where our properties are situated, and given the length of time (in which to repay debt), I like our chances that business will recover in that period,” he says.

Unlike Station Casinos, Planet Hollywood, Riviera and other companies in or near bankruptcy, Harrah’s hasn’t missed any payments of interest and principal on its debt. And yet, it has often paid bondholders millions less than they were owed. Some analysts call this a form of backing out on debts. Harrah’s calls it hard-nosed negotiating that yields something of value for both sides.

These “debt exchanges” have become a popular means of refinancing for overleveraged companies in a recession, especially in worst-case scenarios involving banks that won’t lend and bond investors who won’t buy.

Station Casinos bondholders rejected a similar exchange, forcing that company into bankruptcy even after its owners offered to inject more equity into the company to help keep it solvent. Without funneling more equity into the company, Harrah’s has managed to exchange blocks of debt multiple times in the past year — a sign that investors would rather get more of their money later than potentially less money if they force the company into bankruptcy today.

In addition to exchanging bonds for ones worth a fraction of face value, Harrah’s also has bought company loans trading at a discount to face value, sometimes retiring the debt. In one instance, it paid $97 million to buy notes with a principal amount of more than $500 million maturing between 2015 and 2017.

The company also has twice refinanced bank loans by issuing billions worth of new bonds, some secured by a first mortgage in certain casinos, and using the money to pay bank loans in exchange for a longer maturity date. Although most of the company’s bank loans don’t come due until 2015, Harrah’s is tackling the problem early.

These strategies have helped the company reduce debt, hovering around $19 billion, by more than $4 billion. That leaves Harrah’s with $450 million in loans coming due this year and next — a workable hurdle, analysts say, as the company is expected to generate more than $1.5 billion a year in earnings, even after double-digit declines amid the recession. Earnings fell about 15 percent in the third quarter and analysts expect a worse fourth quarter, as competitors in smaller markets nationwide where Harrah’s has casinos have reported poor results in recent days.

Halkyard’s take is: “Companies don’t go bankrupt because of poor earnings; they go bankrupt because they run out of cash.”

Harrah’s financial outlook gets murky in 2013. That’s when about $5.8 billion of debt comes due. It has gotten a little bit of a head start on that. It had been $6.5 billion until the company repurchased nearly $1 billion of it in recent months for a price analysts say was close to 20 cents on the dollar.

Reflecting longer-term risk, Harrah’s bonds have some of the highest interest rates in the gaming industry. Higher, even, than MGM Mirage, which also narrowly escaped bankruptcy last year and has billions of debt on top of its newly opened, $8.5 billion CityCenter resort that’s competing head-to-head with other luxury resorts in a tough economy. Some of these Harrah’s bonds trade at 60 cents on the dollar versus more than 80 cents on the dollar for MGM Mirage, for example.

The company’s relative silence on its refinancing scheme probably hasn’t helped. Since the company went private, it no longer hosts conference calls with investors. It’s financial statements are Byzantine, reflecting multiple operating companies and debt strategies.

“They’re extremely opaque with investors. They’re not out there telling their story,” Farrell said. “A lot of bondholders won’t invest with them.”

Silent or not, though, Harrah’s executives “are going to need a big recovery in operations just to refinance their debt” in the years ahead, says Chris Snow, a gaming, leisure and lodging analyst for bond research firm CreditSights.

“Are they doing a lot better than they were a year ago? Yes. Are they out of the woods yet? No. If it takes a lot longer for the economy to recover, they’re not going to be able to pay off that debt.”

Halkyard likes the company’s odds.

“You shouldn’t dismiss the ability to buy time,” he says.

Join the Discussion:

Check this out for a full explanation of our conversion to the LiveFyre commenting system and instructions on how to sign up for an account.

Full comments policy